What is the debt snowbank method and why it matters

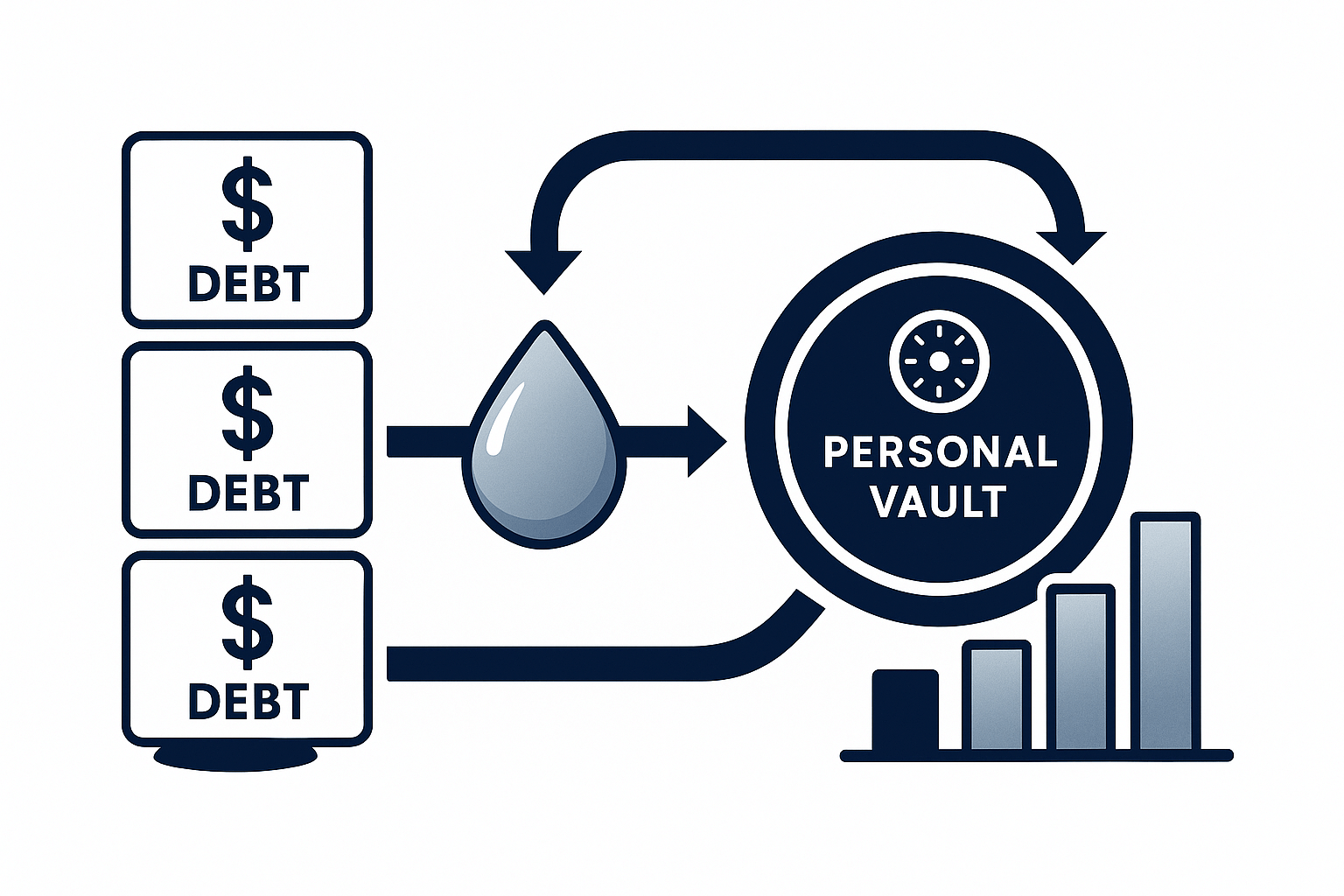

The Debt Snowbank Method is a disciplined way to replace expensive outside debt with policy loans from your own Bank On Yourself plan. You “buy back” your liabilities one by one. Payments that once went to banks now cycle back to your policy, strengthening your balance sheet. The outcome is more control, lower volatility, and interest that benefits you.

This approach builds on a familiar idea. Many owners know the debt snowball, which knocks out balances from smallest to largest. Snowbank focuses on cash value leverage and policy design. You still prioritize momentum, but you also measure opportunity cost, tax treatment, and the timing of premium funding.

If you carry credit cards, merchant cash advances, or variable lines that sting when sales dip, this method can change your stress level quickly. It will not happen overnight. It is not a get rich quick scheme. It is get rich for sure, because the rules run in your favor when you keep them.

Step 1, list and rank every debt

Start with a simple spreadsheet. Capture each balance, the stated APR, compounding method, payment amount, and due date. Add one more column for cash flow pain. High payment and high volatility move a debt to the top. Another column tracks prepayment penalties or fees. This helps you avoid surprises.

Rank by effective rate and pain, not by emotion. A small, low rate loan that annoys you should not jump the line against a merchant advance charging the equivalent of 40 percent. Momentum matters, but math pays the bills. Sorting this list with calm clarity is the first win of the process.

Owners who complete this inventory often find two or three debts that no longer serve their plan at all. Those become prime targets for the first refinance.

Step 2, design the policy that powers the snowbank

Meet with a Bank On Yourself professional to design a dividend paying whole life policy that emphasizes early cash value. You want capacity for paid up additions, a premium you can fund comfortably, and a design that stays within IRS limits. The policy is your private line of credit.

If you already own a policy, request an in force illustration to confirm loan provisions and current dividend assumptions. Do not chase the highest illustration. Choose stability, strong guarantees, and a company with a long track record of paying dividends through many cycles.

Map premiums to your profit rhythm. This helps you fund consistently, which is the heart of compounding. You are building a reservoir, not a slot machine.

Step 3, seed the policy and set banker’s rules

Fund your first premium and paid up additions. While you wait for initial cash value to post, write your banker’s policy. Set a target interest rate for internal loans, a default amortization schedule, and rules for skipping or catching up payments when seasonality hits. Professionalize the process.

Decide who approves policy loans and who records repayments. Even in a one person shop, roles matter. You are teaching yourself, and your team, to think like a lender. That mindset shift is where much of the value lives.

When your policy first becomes loan eligible, resist the urge to drain it. Start with the single worst debt. This is about long term efficiency, not instant relief.

Step 4, refinance the most destructive lender first

Request a policy loan for the amount needed to retire your top ranked debt. Pay that lender in full if possible. Then redirect the exact same monthly payment to your policy loan. You have not increased cash outflow. You have changed the destination. Interest that used to enrich a bank now strengthens your policy and future options.

Track this in your spreadsheet. Note the new policy loan balance, the chosen rate, and the planned payoff date. Put payment reminders on the calendar. Treat your own bank with the seriousness you demanded from yourself when outside lenders were watching.

Owners often feel a surge of confidence after the first refinance. The payment did not vanish. It just came home. That emotional win fuels the next step.

Step 5, rinse and repeat through the list

As the first policy loan balance drops, prepare the next refinance. Keep premiums and paid up additions flowing. Each cycle grows your policy base, which increases the reservoir you can draw from in the future. Over time, interest saved and dividends earned can create meaningful spread in your favor.

Keep a healthy operating reserve outside the policy. This prevents forced loans for minor surprises. The snowbank method is about control. It is not about starving your cash cushion to look clever on a spreadsheet.

Update your ranked list quarterly. Rates change. Business needs evolve. You will make better decisions when the facts are fresh.

How to integrate taxes and legal safeguards

Coordinate this plan with your CPA. Interest on policy loans is usually not deductible, but the interest you eliminate from certain outside debts might be. Basis, dividends, and policy classification all matter. You must avoid MEC status if you want maximum flexibility. Ask for written confirmation each year.

Set up simple internal controls. Record loan requests and approvals. Reconcile repayments monthly. If you have partners, add a brief policy banking clause to your operating agreement so everyone understands the rules.

These steps protect relationships and keep the flywheel spinning. Clarity is kindness when money is moving.

What results to expect and when

In the first three to six months, expect clarity and one refinance. Cash flow stress usually drops here. By month twelve, many owners have retired two or three high cost lenders and redirected several thousand dollars of monthly payments to their own policy.

Across three to five years, the compounding effect becomes obvious. Your policy base is larger. Your access to capital is faster. Your debt structure is simpler and cheaper. You have turned liabilities into a system that serves your goals.

Pair this with strategic authority building to grow top line opportunities. Publishing a book that attracts ideal clients can make each borrowed dollar produce more. See our guidance on client acquisition through publishing and listen to owner stories on the Publish Promote Profit Podcast.

Common pitfalls and how to avoid them

Skipping repayments. Flexibility is a feature, not a loophole. Put missed payments on a catch up plan. Do not normalize delays.

Underfunding the policy. Small premiums produce small reservoirs. If the method matters to you, fund it like it matters.

Chasing shiny illustrations. Base your plan on guarantees. Let dividends be a bonus. Markets and rates will move.

Draining cash reserves. Keep an operating buffer. Forced loans create avoidable stress and fees.

Frequently asked questions about the debt snowbank method

Does my policy stop growing if I take a loan. No. The company lends against your cash value. Your policy continues to earn interest and potential dividends on the full cash value according to the contract.

What happens if I die with a loan outstanding. The loan balance and any interest due are deducted from the death benefit. Heirs receive the net amount. This is why many owners keep repayment steady.

What if my business hits a rough patch. You can reduce or pause payments temporarily. Communicate with your advisor, then catch up as sales recover. Build this flexibility into your written banker’s policy.

The one sentence summary

The Debt Snowbank Method helps you buy back your most painful debts with a policy you control, redirect the same payments to your own system, and compound the benefits for future opportunities.

If you want a complementary strategy that builds pipeline while your finances stabilize, read our latest articles on authority marketing and learn how our authors use a book to move from hunting for clients to being the hunted on the podcast.

Ready to Become a Published Author?

Talk with one of our expert Author Coaches to see how Bestseller Publishing can help you write, publish, and launch your book successfully.

Schedule Your Free Strategy Call

{kind=link}

{kind=link}